—Based on analysis compiled by Andrii Glushchenko, published by GMK Center

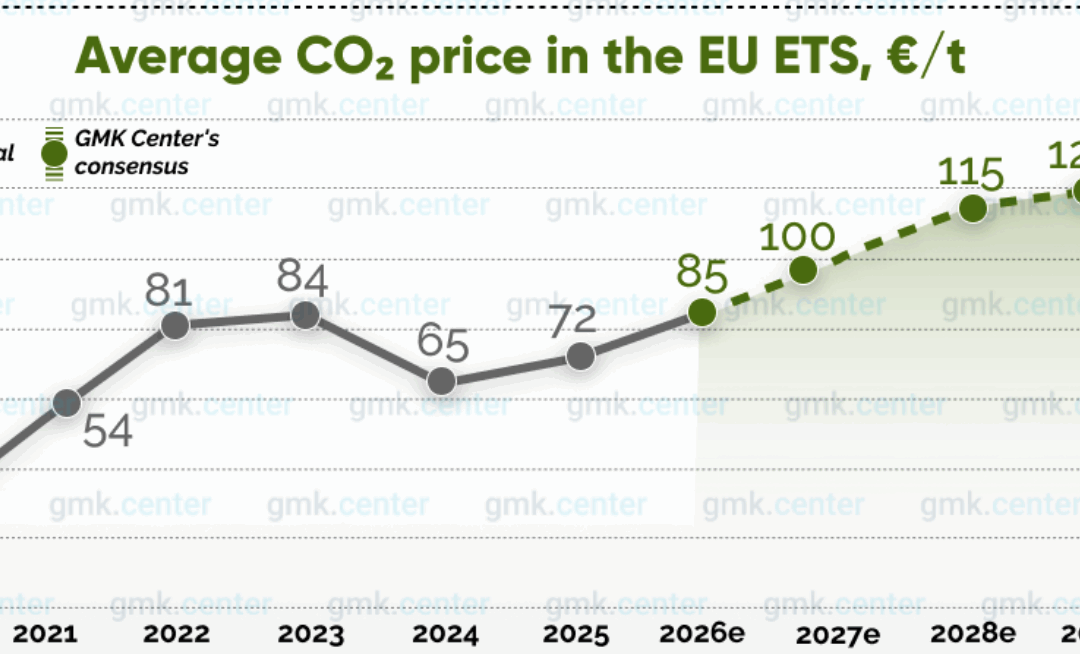

A new consensus forecast from leading research institutions indicates that carbon prices in the EU Emissions Trading System (EU ETS) could rise to €126 per ton of CO₂ by 2030. The projection aggregates outlooks from BloombergNEF, Refinitiv, ICIS, S&P Global, Aurora Energy Research, and the Potsdam Institute, showing ongoing regulatory tightening and uncertainty around Europe’s decarbonisation trajectory. While institutional estimates range widely, from €80 to €147 per ton, the median converges on a steady upward trend as the EU accelerates climate policy implementation.

The expected rise is closely tied to multiple regulatory shifts due to take effect before 2030. In 2026, EU ETS benchmarks will be revised downward and the CBAM will enter full operation, both of which will significantly reduce free allocation volumes. Sectors without strong carbon-leakage exposure will begin receiving just 30% of allowances for free in 2026, with free allocation ending entirely for these sectors by 2030. Analysts also anticipate that the Market Stability Reserve may be strengthened to absorb surplus allowances more aggressively, potentially supporting higher EUA prices. Finally, elevated gas prices that incentivise a switch back to coal may further increase emissions and EUA demand.

Although upward pressure remains dominant, several factors could moderate price growth. Industrial decarbonisation projects supported by EU subsidies, the continued expansion of renewable power, and potential future integration of permanent carbon removal credits into the ETS could offer limited alternative compliance pathways. However, most experts consider these dampening effects insufficient to alter the broader upward trajectory before 2030. EU carbon prices already exceeded €80/t in November, boosted by improving sentiment in energy-intensive industries and Germany’s plans to lower electricity costs for key sectors starting in 2026.

FACS Perspective

The emerging consensus show a simple reality: companies exposed to EU ETS and CBAM must prepare for structurally higher carbon prices through 2030. Declining free allocation, tighter benchmarks, and volatile energy markets will increase cost exposure, making accurate forecasting and proactive hedging strategies essential. At FACS, we view the continued upward trend as a call for industrials, traders, and importers to invest early in emissions measurement, procurement planning, and risk management systems. As further regulatory details emerge in 2026 firms will gain greater clarity to refine their carbon cost strategies and navigate Europe’s evolving market with confidence.

You can read the full GMK Center analysis here: